Solving for a stagnant Indian Capital Market

It requires different innovation for investors and traders

With a population of 138 Crore, India sees only 7 Cr people involved in the capital markets. This is a 5% penetration. Internet penetration in India is about 55% and eCommerce stands at 4.7%.

In 2010, eCommerce was starting up, and Capital Markets had 2% penetration. eCommerce would touch 11% penetration in 2024 whereas there is no such impressive projection for Indian Capital Markets.

To boost capital market penetration, there has to be a focus on two types of participants - investors and traders. Both these participants have two core requirements — 1) ease to execute products which are 2) backed by quality research. This is over and above financial awareness and trust.

One of the biggest roadblocks for new participants is their inability to conduct their own research. This problem is mostly solved for investors but not traders.

Let's analyse below.

Investors

Mutual funds industry played a significant role in increasing investor participation. AMFI, mutual funds AMCs, brokers, banks spread awareness and made it accessible.

Mutual funds are simple to buy and have fund managers and large teams for research. This has enabled crores of investors to participate in capital markets.

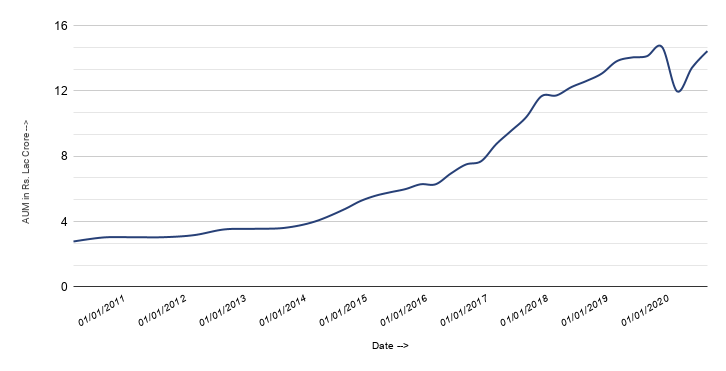

However, the growth in AUM has been flattening for last 2 years.

This means that we need newer products & solutions to sustain growth. Many companies have attempted to innovate but failed, most notably Robo Advisors.

The fall of Robo Advisors

In 2015, there was a rise of robo advisors, and many of them are now dead or merged with larger players.

These companies faced two problems — a very high customer acquisition cost and inability to generate meaningful revenue once the customer is acquired. Most robo advisors do not charge for their service. Their source of revenue is commission income from selling stocks, mutual funds, bonds, insurance.

Assume it costs Rs. 1000 to acquire a customer. Commission on a mutual fund is ~0.8% on the average AUM the customer maintains in a year. To breakeven, this AUM is Rs. 1.25L.

As on September 2020, contribution of retail investors to mutual funds AUM is Rs. 5,60,824 Crore and total folios (a proxy for the number of investors) is 8,40,94,279. Therefore, average AUM per folio is Rs. 66,690. This is half of the required AUM to breakeven.

Therefore, it takes robo advisors 2 years to breakeven just on the acquisition. Add the cost for product development, re-engagement marketing, salaries, and the breakeven times are as high as 4 years.

Bigger players (like banks, stockbrokers) quickly replicated this product to worsen the problem for robo advisors.

Wealthy investors are not included in the above analysis because the majority still invests via banks or relationship managers. INDWealth is on a similar path as CRED to target the top percentile population. But it might face problems with respect to business model just like other robo-advisors.

Despite the lack of a business model, there is impressive product innovation — Simplified SIPs, digital KYC, single-click execution of mutual funds (or basket of stocks). Both old and new companies adopted these features. This has solved for simplicity in execution which is a core requirement of investors.

As for research - brokers, banks actively engage in providing quality research for investments. With the rise of players like IndWealth and Smallcase, independent institutions and individuals can also engage in this activity to benefit investors.

Therefore, investor's two core requirement (research and simplicity of execution) is in the process of being solved, and a rich ecosystem is building.

But this is still not sufficient to mobilise the next wave of investors. Nithin Kamath's blog on how to improve investors’ participation is a must-read. TLDR:- He believes that the next surge of participation will come from products that offer the safety of fixed deposits but assured higher returns. They are interested in funding this problem.

Traders

Zerodha, Upstox, 5Paisa, Aliceblue and other discount brokers have had a significant impact on traders.

First is pricing disruption by slashing brokerages to 1/100th of then-existing levels meant a much lower requirement for breakeven returns. This opens up a lot more trading opportunities.

Second is the improvement in experience while trading. No longer are traders required to see tiny white numbers on a black screen, which can be daunting. The information is now better presented, and few features to prevent traders from making errors.

The third is broker APIs that allow tech-savvy traders to automate order execution.

All these factors combined encourages more people to try trading, and it is working. After flat growth in the early years, number of active clients with brokers is rising.

However, all brokers are continually fighting to keep acquiring new traders as most of them become inactive after sustaining losses.

Let's work backwards and ask two questions.

How many traders can design their own strategies successfully?

How many traders can use APIs?

The answer to both questions is tiny.

There are two types of products available that try to address this gap — Do-it-Yourself (example Streak, Sensibull) or Community Driven (example Tradetron, Kuants).

Do-it-Yourself (DIY) products expect the trader to be proficient in building strategies. They do not require coding skills; however, the traders should possess immense knowledge about technical indicators. Most experienced traders will struggle in using these products. Additionally, technical analysis based trading is outdated. They were designed in the 1970s and do not perform well in today’s information and computing age.

On the other hand, Community Driven products are a sinkhole for anyone to publish strategies. Whenever a trader wants to select a strategy, they have to choose between between 100s of complex sounding names & numbers.

All newbie and most professional traders find it challenging to find the best strategy for themselves.

Ultimately, both solutions, again, just solve for a fractional market and do not have a mass-market appeal.

For investors, where research and order execution is available in a tidy end-to-end service from robo-advisors like services, we need to offer something similar to traders.

A solution that significantly reduces the cognitive load of traders will have a mass-market appeal. But beware the regulatory challenges.

Traders are intrinsically motivated to trade as compared to investors who invest. Whereas a new product for investors requires predictability, it should provide a safe & structured environment for traders when pursuing high risk/returns.

A final observation is that we need new products to attract new investors, but we need new products to re-engage existing traders.

Your thoughts below are welcome.

Reach out to me at salil@yobee.co.in or Twitter

📧 🐦

—

Salil Mathur